Medicaid Planning / Asset Protection

Medicaid Planning/Asset Protection

Serving Clients in New York City and the New York Metropolitan Area

Are you or a loved one faced with long-term care expenses? Is the cost of long-term care, nursing homes, assisted living, and home care getting to be too much?

If you are thinking about Medicaid, you should speak to an attorney who specializes in that area of law as soon as possible. There is really no time to waste – all you are wasting is money and adding stress. The sooner you get going on a workable care plan, the sooner your stress will be reduced. You may also learn that you are eligible for Medicaid benefits.

When we hear the word “crisis,” we think of disasters or calamities of epic proportions. Well, that is where many Americans find themselves when they (or a family member) try to stay above water financially when dealing with the excessive costs involved with senior care – especially when residential facilities are involved.

Accordingly, “crisis planning” in this context is planning for those who have an imminent need for extensive chronic health care services and may need Medicaid benefits.

What if Your Spouse Has a New Diagnosis?

Along with the devastating news, the physician recommends that they may need to be placed in a nursing home. You have no idea what this will cost, let alone how you will pay for it. In short order, you learn that Medicare will not cover the long-term needs. You become familiar with Medicaid but have no idea whether your spouse qualifies or even how to apply. You need to discuss the Medicaid planning and the application process with our firm’s experienced elder law attorneys. An elder law attorney will have the necessary skills and contacts to help you create a strategy, engage and direct healthcare providers, and work with you to apply for Medicaid and secure needed benefits.The elder law attorney will get your application approved and implemented.

Does Medicare cover nursing home bills? Unfortunately, only in a limited way.Medicare still remains somewhat of a mystery to most Americans, like the hypothetical couple above. Many people are under the impression that Medicare will cover all of the expenses for nursing home care.

That is not the case. Medicare may cover the first 100 days, and this may be limited, if you are even eligible at all. You must receive skilled nursing care in a nursing home, such as physical or occupational therapy. Medicare is not related to income or resources. Most retired workers over 65 and certified disabled workers are eligible for Medicare.

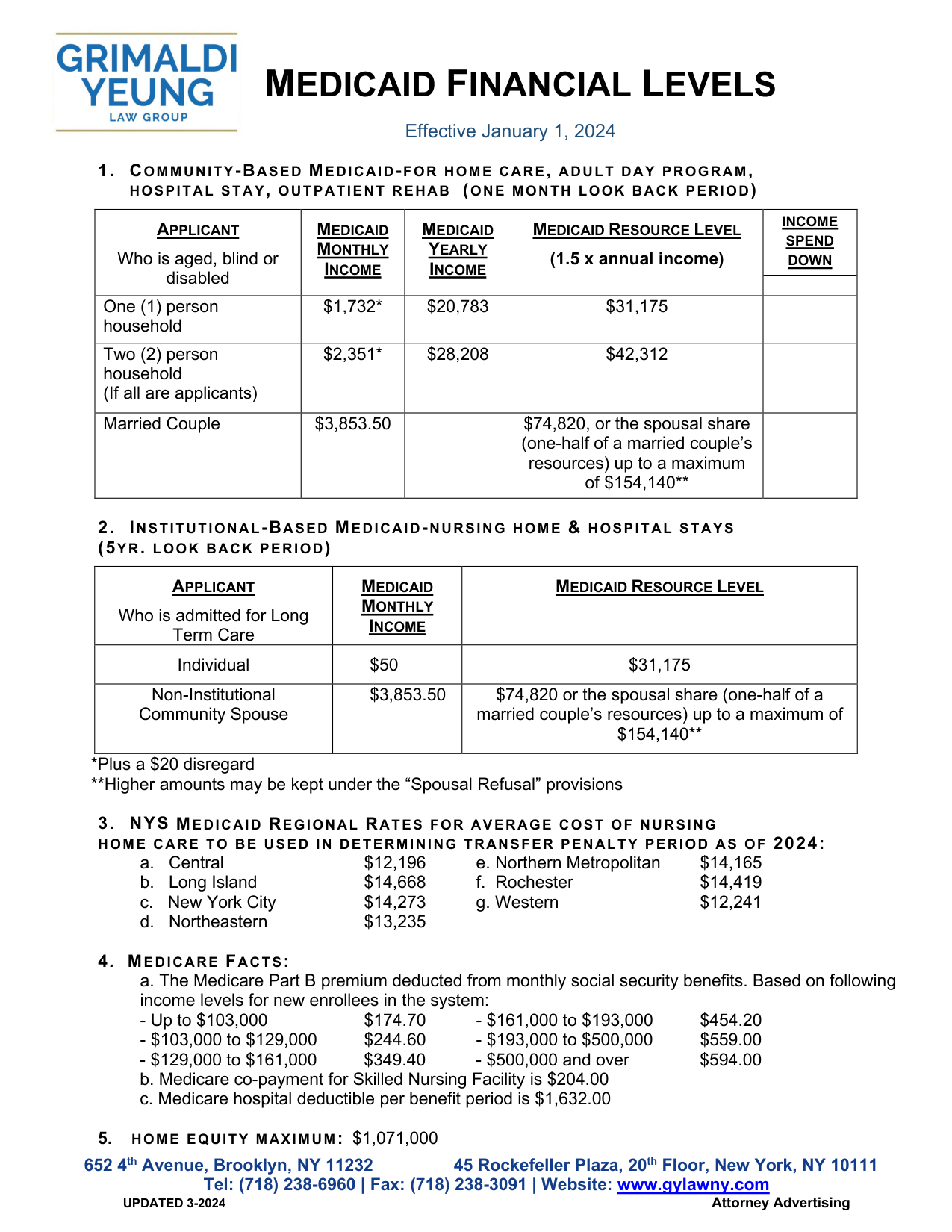

So where does Medicaid come in? For most people, Medicaid becomes an option after Medicare benefits are exhausted. Many people don’t realize that Medicaid benefits are not automatic. In fact, to receive Medicaid, a patient and the patient’s spouse (if married) must first “spend down” their “countable” assets. In other states that limit is down to $2,000 but gets more complex for married couples. New York’s resource limit is more generous and increases annually to coordinate with Cost of Living adjustments. You may view the current limits HERE. There also are categories of assets that will be automatically exempt for purposes of Medicaid qualification. There are also spousal income and asset exception rules for married couples when only one spouse is applying for benefits, as not to impoverish the community/well spouse.

{kind=link}

It sounds pretty easy, right? Wrong! Actually, things can get complicated quite quickly. What do I do to protect my assets? What do I do to convert assets without affecting my Medicaid eligibility? Do I apply before or after we start getting care (and bills?)

These are all valid questions, and rather than attempting to answer them on your own with everything else that is swirling around you, you should seek professional advice from a qualified attorney who practices in Medicaid planning, understands the Medicaid system, and can help you get organized for the future. If you qualify, Medicaid benefits can help pay for certain medical expenses such as:

•Doctor and Hospital Bills

•Prescriptions

•Vision and Dental Care

•Medicare Premiums

•Nursing Home Care

•Personal Care Services (PCS), Medical Equipment, and Other Home Health Services

•In-Home Care under the Community Alternatives Program (CAP)

•Mental Health Care and the majority of medically necessary services for children under age 21

We are all most vulnerable in circumstances when we “don’t know what we don’t know.” Know your legal rights and make care of your loved one more affordable.